S.BOLD-ERDENE

bolderdene@mininginsight.mn

- Is the USD 30 billion contract signed in the tent not important? -

The highlight event of Mongolia’s mining sector in May was the historic agreement signed between Erdenes Tavan Tolgoi (ETT) and China Energy. Considering it is a 20-year, or even longer-term contract, with a value of at least USD 30 billion, it can only be described as a historic agreement. On May 14, during the inauguration of the border connection railway construction, ETT signed a long-term coal sales and purchase agreement and a general cooperation agreement to increase mine capacity with China Energy Group of China. The signing was done by Kh. Munkhjargal, Acting CEO of ETT, and Yu Chuan, Chairman of the Board of China Energy International Development LLC. These two agreements can be considered as the “payment” for building the border connection railway. The only requirement was that the Chinese side had to sign three agreements together in order to construct and connect the border railway. Although this agreement was at the center of political and business attention for a considerable period, especially in the past year, the signing ceremony was modest and quiet.

Photo: A long-term agreement signed with a Chinese state owned company 14 years after “Chalco” deal.

Whether the ceremony was overshadowed by the noise surrounding the railway construction or there was a deliberate avoidance of a grand ceremony to widely publicize it is interesting to note. Considering the content, monetary value, and economic importance of the agreement, a grand ceremony comparable to that of the Oyu Tolgoi agreement or the Orano Mining agreement could have been held. At least, a modest ceremony like that of the Chalco agreement 13 years ago was not even held. This seems to indicate that the government gives more importance only to the border connection railway while somehow avoiding discussing the agreements of ETT. Even the announcement hanging in the room where the contract was signed is gloomy. It is unclear who signed the agreement with whom, as if it was deliberately concealed. The most important agreement among the two mentioned above is the long-term coal sales and purchase agreement. This is because the agreement was signed at a time when coal prices were sharply declining. Moreover, the price was revised from the initially discussed terms and set to be calculated using the pricing methodology of the Chalco agreement, which poses a risk of negative consequences similar to those of the previous Chalco contract.

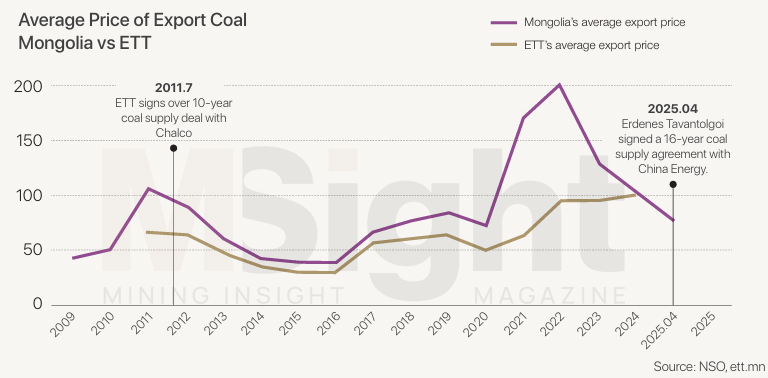

The graph below clearly shows the export coal prices at the time the agreements with Chalco and China Energy were signed. Mongolia’s coking coal export history began in 2004. By 2011, when the average export price reached its highest point of USD 106.7, ETT started its export operations. In July of the same year, ETT signed a long-term agreement with Chalco. The initial contract price was USD 70, which was more than 30% lower than the average export price of that year. Since then, Mongolia’s coal export price remained below USD 100 until 2021, while ETT’s average export price did not exceed USD 70 until 2022. In 2016, the national average price dropped to USD 37.7, ETT’s average price to USD 28.1, and Chalco’s price to USD 28, marking the lowest point. Conversely, in 2022, the national export average price peaked at USD 202, and ETT’s average export price reached its highest point of USD 102 in 2024. The sharp rise in ETT’s price was largely influenced by selling coal through the exchange and based on border conditions. Since 2022, the national average export price has been declining, with the average price for the first four months of this year at USD 77. Signing a long-term agreement at a time when export prices have significantly dropped, indexing the price, and tying it to mine amortization conditions may result not only in stagnant or declining coal prices but could also have a considerably negative impact on ETT’s sales going forward.

The graph below clearly shows the export coal prices at the time the agreements with Chalco and China Energy were signed. Mongolia’s coking coal export history began in 2004. By 2011, when the average export price reached its highest point of USD 106.7, ETT started its export operations. In July of the same year, ETT signed a long-term agreement with Chalco. The initial contract price was USD 70, which was more than 30% lower than the average export price of that year. Since then, Mongolia’s coal export price remained below USD 100 until 2021, while ETT’s average export price did not exceed USD 70 until 2022. In 2016, the national average price dropped to USD 37.7, ETT’s average price to USD 28.1, and Chalco’s price to USD 28, marking the lowest point. Conversely, in 2022, the national export average price peaked at USD 202, and ETT’s average export price reached its highest point of USD 102 in 2024. The sharp rise in ETT’s price was largely influenced by selling coal through the exchange and based on border conditions. Since 2022, the national average export price has been declining, with the average price for the first four months of this year at USD 77. Signing a long-term agreement at a time when export prices have significantly dropped, indexing the price, and tying it to mine amortization conditions may result not only in stagnant or declining coal prices but could also have a considerably negative impact on ETT’s sales going forward.

HOW IS IT DIFFERENT FROM THE CHALCO AGREEMENT?

In July 2011, ETT signed a long-term coal supply agreement with the Chinese company Chalco Trading. This agreement involved receiving an advance payment of USD 350 million, which was to be repaid through coal deliveries. The agreement was extended for five years in 2022. To repay the advance payment of USD 350 million along with interest, about 25 million tonnes of coal were supplied, with full repayment completed in 2017. The Chalco agreement is characterized primarily as an advance payment contract. In contrast, the China Energy agreement does not involve any advance payment; rather, it covers mine investment, operations, and sales. ETT will pay MNT 860 billion in cash for the financing of the border connection railway constructed by a subsidiary of China Energy. Information about the two agreements between ETT and China Energy remains confidential. Here, some details are shared with readers about how previously discussed terms have changed and how criticisms raised by the Parliament and the public have been addressed.

CONTRACT PRICE

The most critical issue that the companies could not agree on in the long-term coal sales and purchase agreement was the price. ETT, following the law, requested to supply coal at the Exchange price, but China Energy insisted on using the pricing terms of the Chalco agreement signed 14 years ago and still in effect. Many factors lie behind this. For example, before last year’s parliamentary elections, the parties had almost agreed on ETT’s price proposal, but after the elections, the Chinese side suddenly changed their conditions.

The rationale was that one Chinese state-owned company had signed a very favorable long term contract with ETT, so another state-owned company could not make a contract on worse terms. Under this pressure, the Mongolian side had no choice but to accept China Energy’s pricing proposal.

There was even a proposal to sign the contract only after the Chalco agreement expired in 2027. However, without amending the law, the price was clearly specified in an intergovernmental agreement between the two countries. The agreement titled “Agreement between the Government of Mongolia and the Government of the People’s Republic of China on Cross-border Railway at the Gashuunsukhait Gantsmod Customs, Coal Trade, and Cooperation to Increase the Capacity of the Tavan Tolgoi Coal Mine” states that “… both parties, considering the benchmark level of the previously signed long term coal sales and purchase agreement, agreed that the last confirmed price will be the initial price (FCA – coal delivery point at the Tavan Tolgoi mine site), and subsequent prices will be determined by a mutually agreed mechanism based on ‘initial price + seasonal index adjustment’…” The price agreed under this international treaty ratified by the Parliament and Government means that domestic legal prohibitions, restrictions, or company policies do not affect the price. If ETT suffers losses due to a price drop similar to that of 2015–2016, Parliament and the Government will have no grounds left for criticism. The initial base price was officially announced as USD 59 during the opening ceremony. Currently, this price is the highest among companies that have signed long term contracts with ETT, so future pricing will be calculated on this basis with indexation. This means that ETT has lost the opportunity to sell coal on the Exchange or under border conditions at a higher price. However, one measure to prevent losses from price declines is that the sales price is not allowed to fall below ETT’s production cost. This clause is particularly significant for thermal coal.

Thermal Coal. The most closely watched issue in the two contracts above was the coal classification. The key question was whether the annual 5 million tons of coal to be sold until 2030, and the additional 20 million tonnes annually to be mined and sold from the new mine totaling 220 million tonnes-would all be coking coal or include all types of coal. Even while the matter was under discussion in the Parliament, there was strong criticism that selectively mining and supplying only coking coal was wrong. The Chalco contract specified only hard coking coal, which led to criticism that the deposit was being selectively mined. The China Energy contract stipulates that 30 percent of the annual coal sales will be thermal coal, with the remainder being coking coal. Here, coking coal also includes semi-coking coal, or one-third coking coal. By including this provision, ETT was able to preserve the possibility of utilizing its deposit without selective mining and gained the advantage of securing a stable long-term buyer for thermal coal.

Contracted Operator. China Energy showed interest in fully managing the exploitation, sales, and transportation of the Bortolgoi and Onchkharaat deposits. However, this could have led to ETT losing control over mine supervision and sales policies, potentially negatively affecting company operations. During negotiations, it was agreed that ETT would be responsible for all “paperwork” such as exploration and feasibility studies for the Bortolgoi and Onchkharaat deposits. Additionally, a legal tender process will be conducted for selecting a contracted operator at these deposits. China Energy’s subsidiary will act as the contracted operator and will work under the same conditions as other contracted operator companies of ETT. The contracted operator’s fees are set to be competitive with those of domestic contracted operators. Although China Energy initially requested to settle operator fees in CNY, it was ultimately agreed to settle in MNT. Coal sales will be managed by ETT, with payments made in USD. As a result, China Energy will no longer enjoy many privileges like Chalco’s contract, such as mining and selling at will or halting production if prices drop. In short, this arrangement avoided public criticism that ETT was giving its two mines to the Chinese.

Coal Transportation. There had been concerns that selling coal on FOB terms would allow Chinese companies to dominate transportation entirely, pushing out Mongolian transport companies and causing job losses. However, by signing a 16-year contract with China Energy, the Tavantolgoi Railway will transport coal by rail from Tavantolgoi to the coal loading and unloading terminal at the Gashuunsukhait border. During this period, O. Batchuluun, CEO of Tavantolgoi Railway, stated that transport profits totaling USD 2.5 billion are expected. Transportation fees will be linked to coal prices and calculated with indexation. If coal prices fall, transportation costs will decrease; if prices rise, transportation costs will increase accordingly. This arrangement essentially eliminates differences in mine FOB terms and border conditions. The advantage is that the transportation costs and profits from the annual export of 20 million tonnes of coal will remain in Mongolia. Thus, a major agreement has been signed that will define the outlook and trajectory of ETT and, by extension, Mongolia’s coal sector-for the next 20 years. Ensuring the transparency of both the agreement itself and its implementation is crucial, at the very least, to prevent the company’s executives from being summoned by law enforcement authorities, and more broadly, to underscore to the Government the importance of stability, as history has clearly shown.

Mining Insight Magazine, May 2025 №05 (042)