- Second Half Aimed at Minimizing “Misunderstandings” -

- Second Half Aimed at Minimizing “Misunderstandings” -

E. MISHEEL misheel@mininginisght.mn

The issue regarding the two licenses of Oyu Tolgoi loosened up just as the government faced dismissal. However, the matter remains unresolved. If the dismissal and reformation of the government drags on, the parliamentary discussion of the profit-sharing agreement concerning the 20% stake held by Entrée within Mongolia’s 34% interest-may be delayed. Meanwhile, according to the underground development plan, Oyu Tolgoi is set to begin operations in Entrée’s licensed area in early June. Should the agreement be stalled, a potential “misunderstanding” may arise at Oyu Tolgoi.

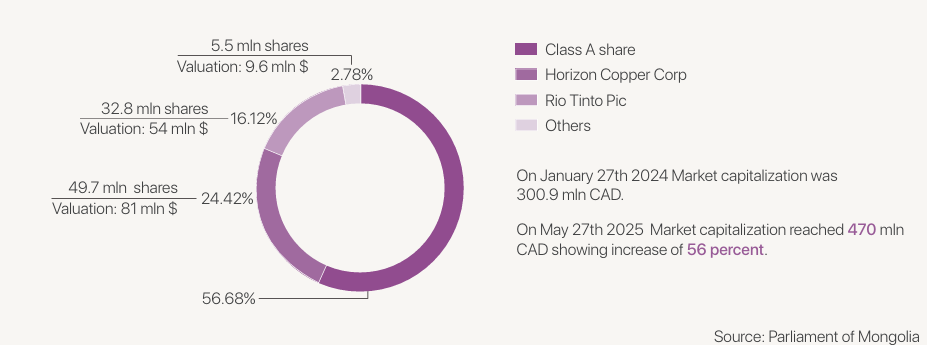

A BRIEF OVERVIEW OF THE AGREEMENT BETWEEN ENTRÉE GOLD AND RIO TINTO

In 2004, Entrée Resources and Turquoise Hill Resources signed a Profit-Sharing Agreement. According to the agreement, if Turquoise Hill Resources invested USD 35 million in geological exploration on Entrée’s license area, the economic benefits from mining would be split 70/30 for depths up to 560 meters, and 80/20 for anything deeper. The USD 35 million investment was made, and the agreement has remained in effect since then. During this time, Turquoise Hill Resources became fully owned by Rio Tinto.

However, as Rio Tinto declined to engage in negotiations on the Profit-Sharing Agreement, Entrée Resources-later renamed Entrée Gold-filed a case with international arbitration in May 2022. The case was resolved in favor of Entrée Gold in December 2024. As a result, the two companies reached an agreement in February 2025 to establish a joint venture, effectively settling the dispute. In essence, the two parties reached mutual understanding within three months since the end of last year. Sources confirm that negotiations over Mongolia’s 34% share related to the 20% owned by Entrée Gold have already begun. Entrée Gold is reportedly keen to reach an agreement with the Mongolian side as quickly as possible, as timely progress on the underground mine would allow them to begin generating profits on schedule.

However, as Rio Tinto declined to engage in negotiations on the Profit-Sharing Agreement, Entrée Resources-later renamed Entrée Gold-filed a case with international arbitration in May 2022. The case was resolved in favor of Entrée Gold in December 2024. As a result, the two companies reached an agreement in February 2025 to establish a joint venture, effectively settling the dispute. In essence, the two parties reached mutual understanding within three months since the end of last year. Sources confirm that negotiations over Mongolia’s 34% share related to the 20% owned by Entrée Gold have already begun. Entrée Gold is reportedly keen to reach an agreement with the Mongolian side as quickly as possible, as timely progress on the underground mine would allow them to begin generating profits on schedule.

CHRONOLOGY OF THE LICENSES

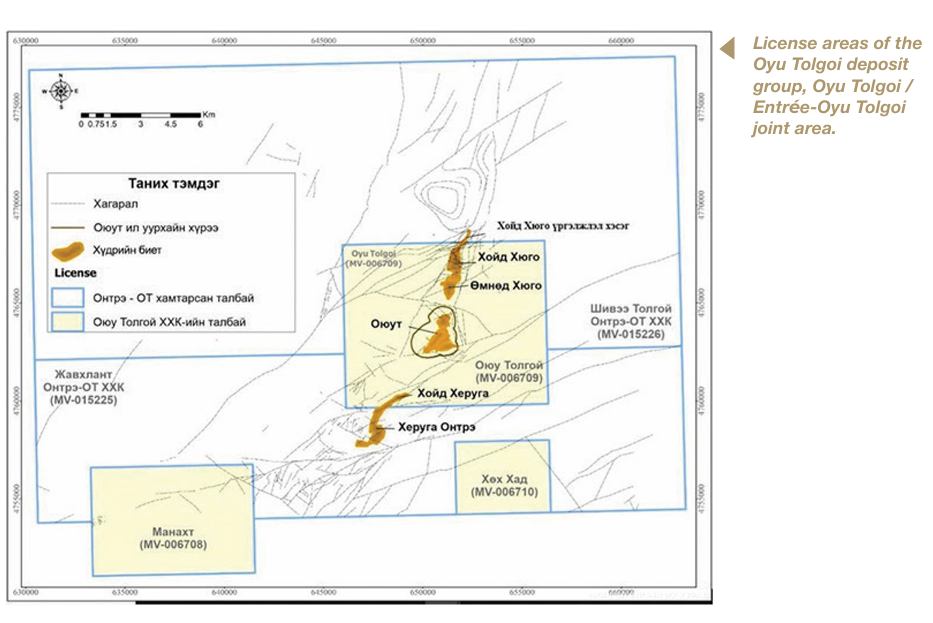

The mining company Entrée holds two mining licenses: “Shivee Tolgoi” (MV-015226) and “Javkhlant” (MV-015225). The exploration license initially issued under the name 3148X (Shivee Tolgoi – MV-015226) was granted to Mongol Gazar LLC on April 3, 2001. Since then, it changed hands twice via Mongol Gazar LLC and MGP LLC, and once each via Bayaraam LLC and Trust-Leasing LLC, before being officially transferred from MGP LLC to its current owner on October 28, 2003.

The other exploration license, 3150X (Javkhlant – MV-015225), was also first granted to Mongol Gazar LLC on April 3, 2001. It passed through Bayaraam LLC and MGP LLC before reaching Entrée on September 30, 2003. Both exploration licenses were converted into mining licenses by Order No. 877 of 2009 issued by the Director of the Geology and Mining Cadastre Division of the former Mineral Resources Authority.

The other exploration license, 3150X (Javkhlant – MV-015225), was also first granted to Mongol Gazar LLC on April 3, 2001. It passed through Bayaraam LLC and MGP LLC before reaching Entrée on September 30, 2003. Both exploration licenses were converted into mining licenses by Order No. 877 of 2009 issued by the Director of the Geology and Mining Cadastre Division of the former Mineral Resources Authority.

RESERVES OF ENTRÉE’S TWO LICENSED AREAS

Oyu Tolgoi’s Hugo North Extension, Panel 1, contains 40 million tonnes of probable production reserves. It has an average copper grade of 1.54%, gold content of 0.53 g/t, and silver content of 3.36 g/t. After 17 years of mine operation, extraction from Panel 1 will be completed, and production will move to Panel 2, which has a mine life of 22 years. According to the preliminary economic assessment, Panel 2 contains 78 million tonnes of indicated geological resources and 88 million tonnes of inferred geological resources, with average grades of 1.35% copper, 0.49 g/t gold, and 3.6 g/t silver. Additionally, the Heruga deposit has an estimated 1.4 billion tonnes of inferred geological resources, with a copper equivalent grade of 0.68%, according to a 2021 estimate. Entrée’s two mining licenses MV-015226 and MV-015225 account for 24% of the copper, 42% of the gold, 29% of the silver, and 94% of the molybdenum content in the Oyu Tolgoi group of deposits. According to Entrée Gold, mining at Heruga-another underground deposit within the Oyu Tolgoi group-will begin in 2031. Prior to that, production will mainly come from the Hugo North underground mine, with the Oyu Tolgoi open-pit mine expected to extract 500,000 tonnes of high grade metals annually starting in 2028. After peak production concludes in 2036, Oyu Tolgoi will continue to produce around 350,000 tonnes of copper annually for the next five years. This is approximately 40% higher than last year’s high output.

WAS THE OVERLAP OF LICENSED AREA OPERATIONS AND CONTRACT NEGOTIATIONS A COINCIDENCE?

Oyu Tolgoi’s majority shareholder has historically shown limited trust in Mongolia’s governing bodies. For instance, in the risk disclosure section of Turquoise Hill Resources’ 2014 year-end report-holder of a 66% stake in Oyu Tolgoi-the company noted that “there is no assurance that the Parliament and Government of Mongolia will not seek to amend or renegotiate the Investment Agreement.” While it is understandable for a company to assess and account for risks, it raises questions about whether this skepticism played a role in delaying agreement on ownership terms with Entrée over the years. Back in 2015, around the time the Underground Mine Development and Financing Plan was approved, discussions were reportedly underway within the government about transferring Entrée Gold’s stake to Oyu Tolgoi LLC or Erdenes Oyu Tolgoi LLC. The latter represents the Government of Mongolia in the project. Just as Rio Tinto and Entrée agreed on a license transfer independently, there may have been opportunities for Erdenes Oyu Tolgoi and Entrée to establish a contract on the 34% share corresponding to Mongolia’s interest. So why did negotiations to finalize the agreement begin just a few months before entering the licensed area? Were various contract scenarios considered beforehand? Or did Mongolia find itself in a passive position-lacking experience beyond the Oyu Tolgoi Investment Agreement-and left to simply await the outcome of discussions between Entrée Gold and Rio Tinto? Despite these questions, the profit-sharing agreement is currently progressing. On the other hand, Mongolia’s economic outlook appears challenging. Researchers are warning that no signs of coal price increases-the country’s main export commodity are evident. Therefore, it has become necessary to proceed with development into Entrée’s Hugo North Extension zone, in line with the project plan, to increase copper grades and volumes gradually ahead of full scale underground production starting in 2027. Given this situation, the timely alignment of license transfers, profit-sharing negotiations, and development schedules can hardly be seen as a coincidence. The Government of Mongolia is expected to establish a profit-sharing agreement with Entrée similar to that of Rio Tinto. However, if Parliament delays the discussion or avoids addressing the agreement altogether, the risk of a “misunderstanding” arising becomes increasingly concerning.

ANOTHER AGREEMENT: TAX DISPUTE TO CONTINUE

Multiple significant developments are converging at Oyu Tolgoi this year. In 2025, the project is transitioning from the underground development phase to production, entering the second half of its 30-year Investment Agreement. There is hope for a resolution to the ongoing tax dispute, and the scheduled seven-year review to potentially reduce the interest rate on the IA loans is also approaching. On the other hand, a renewed tax dispute may be on the horizon. According to the Minister of Economy and Development Ts. Tuvaan, during a press briefing on April 25, 2025, Mongolia’s tax authorities are auditing Oyu Tolgoi’s accounts for the 2020–2025 period, and again, figures in the trillion MNT range are under discussion. He stated: “Between 2013 and 2020, Mongolia froze and used MNT 1.3 trillion related to a tax dispute. Now, the 2020–2025 audit is underway, and a penalty in the trillion MNT range is being discussed. Two working groups have been formed to negotiate with Oyu Tolgoi. Despite holding a meeting a week ago, no solution was reached. This may require amendments to the Law on Legislation, the Law on Investment, the Law on International Treaties, and the General Tax Law. One possible obstacle to resolution is a clause related to double taxation.” In parallel, Mongolia may seek to lower the IA loan interest rate and explore the possibility of selling its share of Oyu Tolgoi’s copper through a commodity exchange this year. Member of Parliament O. Batnairamdal explicitly raised these issues in an interview published on May 8, 2025. He stated: “Entrée operates under financing terms similar to ours at Oyu Tolgoi, yet it enjoys an interest rate 4.5% lower. Furthermore, while we lack the right to sell our 34% share of the copper concentrate, Entrée signed a sales agreement with Rio Tinto this February granting them such rights.” In conclusion, the status of the long-discussed agreement with Entrée-ongoing for more than a decade-remains unclear within Mongolia. While preparing this article, inquiries were sent to the relevant parties and ministry officials, but no response was received. At this stage, there is little choice but to hope that Mongolia’s representatives can negotiate the inclusion of favorable terms from the Rio Tinto–Entrée agreement into the 34% contract concerning Entrée’s 20% share, and even integrate some of these terms into the Oyu Tolgoi Investment Agreement itself.

Mining Insight Magazine, May 2025, №05 (042)