ARIUNTUYA.N

ARIUNTUYA.Nariun@mininginsight.mn

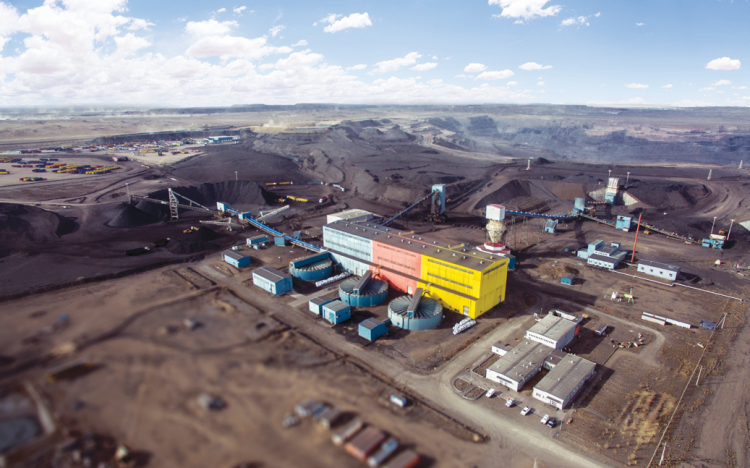

Mongolia is on the verge of signing its second Investment Agreement (IA) after 14 years, following the Boroo Gold and Oyu Tolgoi agreements. Leading the negotiations for the IA with Orano are Ministers Nyambaatar. Kh and Amarbayasgalan. D. If Orano's IA is approved, they will be the architects of this contract, possibly facing a destiny similar to the authors of the Oyu Tolgoi Agreement, who believed in the merits of their deal but encountered strict conditions. While there are several similarities between the two agreements, there are also significant differences. Oyu Tolgoi's investor is Rio Tinto, one of the world's top two mining companies, whereas Zuuvch-Ovoo's investor is Orano Group, one of the world's top three uranium companies.

Notably, one is a major multinational private corporation, while the other is a state-owned enterprise majority-owned by the French Government. First and foremost, the joint venture with Orano Mining represents a "smaller" project in terms of investment and its impact on the Mongolian economy and macro-environment compared to Oyu Tolgoi. Oyu Tolgoi stands as a USD 15 billion project, whereas Zuuvch-Ovoo has an investment of USD 1.6 billion, which is roughly ten times smaller.

Additionally, it lacks investment flow and economic activity on the scale of Oyu Tolgoi. Despite its disparity in economic impact, IA of the Uranium project introduces new investments, mineral products, and export destinations in the third neighborhood. While Mongolia has a history of uranium mining, this current endeavor marks a significant departure from the past. In the previous century, uranium mining was directed towards our northern neighbor due to their influence and power, rather than aligned with national interests and development policies. Mongolians had no involvement in this production at the time. However, now, by establishing the Orano IA, Mongolia is officially becoming an active participant in uranium production. In this regard, it represents a project aimed at diversifying the mining industry, introducing new types of minerals into the economic circulation, opening new avenues for exports, spurring subsequent mining activities, and encouraging uranium exploration. Moreover, it positions Mongolia for greater recognition and prominence in the field of nuclear energy, holding significant economic, political, international relations, and geopolitical implications. Considering the current landscape, there is a growing demand for minerals deemed crucial for the transition to clean energy. Several countries are incorporating uranium into their lists of strategic raw materials or critical minerals, and there is a potential for price growth in the uranium market. As the moment approaches to draft the Memorandum of Understanding (MoU) to establish a new special relationship, it is natural to inquire about the lessons learned from the initial agreement, the corrections and changes made, and the preparations for the upcoming agreement.

LESSONS LEARNED FROM OYU TOLGOI, SPECIAL ROYALTY TERMS

The Oyu Tolgoi Agreement, established at the end of 2009, marked a wholly new experience for our country. In contrast, the Zuuvch-Ovoo's Investment Agreement (IA) is grounded in substantial lessons and experience. Over the course of 14 years, Mongolia has examined the Oyu Tolgoi IA, engaged in discussions with the public, and the debates surrounding it continue to this day. Hence, the foremost condition for forming a joint venture with Orano Mining is the Mongolian Government's decision to relinquish the 34 percent ownership, which was at the core of the disputes related to Oyu Tolgoi, and instead replace it with a special royalty. This adjustment reflects a valuable lesson learned from the Oyu Tolgoi agreement. In general, the regulations concerning additional and special royalties introduced in the Minerals Law since 2010 are all inspired by the Oyu Tolgoi Agreement. Just one year after the signing of the investment agreement, amendments to the Minerals Law were made in November 2010 to include provisions on receiving additional royalties. Subsequently, in September 2011, the Government of Mongolia approached the management of Ivanhoe Mines and Rio Tinto, requesting negotiations to incorporate Oyu Tolgoi into the additional royalty framework. However, they were met with the reminder that the carefully crafted agreement had little room for further revisions. In 2015, special-purpose royalties were introduced, marking a strategic move by the Government of Mongolia to break the deadlock in negotiations with Oyu Tolgoi investors. The initiator of this measure was Bayartsogt. S, the architect of the Oyu Tolgoi agreement, aiming to address the issue surrounding the 34 percent ownership. As a reminder, former Prime Minister Saikhanbileg. Ch sought the opinion of the citizens through a mobile poll regarding the appropriateness of bringing strategic deposits into economic circulation. Over 50 percent of all citizens voted in favor. In response, shortly after the Prime Minister disclosed the poll results, the Minister of Mining and Heavy Industry submitted a draft law amending the Minerals Law to the Speaker of the Parliament on February 6, 2015. Within 12 days, the legal framework for replacing state-owned shares with special royalties was established through amendments to the Minerals Law on February 18, 2015. On several occasions, the Government of Mongolia expressed readiness to negotiate the exchange of the 34 percent ownership of Oyu Tolgoi with special royalties, instead of the original plan to transfer state ownership of strategic deposits to investors in exchange for a special payment. However, this option was not discussed. The additional and special royalty arrangements, initially devised as a solution for Oyu Tolgoi's obligations, have now become the guiding principle for the Orano IA, akin to a golden opportunity. These provisions, which aimed to create a favorable environment for reconsidering the Contract of Guarantee (CoG) for Oyu Tolgoi and developing Gatsuurt and Tavan Tolgoi, have today become the savior for the Working Group tasked with negotiating the CoG with Orano, chaired by Ministers Nyambaatar. Kh and Amarbayasgalan. D, protecting them from potential political repercussions.

Without these provisions, the only viable option today would have been to retain 34 percent ownership, invest USD 500 million, and borrow from Orano, akin to a version of Oyu Tolgoi with reduced monetary value. Thanks to these provisions, the issue of freezing and compromising on tax payments is no longer on the table. This represents a crucial lesson derived from Oyu Tolgoi, and regardless of its origin, it is commendable that it was implemented. If the deal with Orano succeeds, this will mark the first application of special royalty arrangements in this context. An issue arises in the application of additional royalties to the Orano CoG due to the omission of uranium from the list of 23 products specified in the Minerals Law for calculating additional royalties. This is because the regulation of uranium, in connection with radioactive minerals, falls under the purview of the Law on Nuclear Energy. However, the relationships pertaining to strategic deposits are governed by the Minerals Law. Uranium is considered a strategic deposit regardless of its reserve size. Furthermore, the Law on Nuclear Energy stipulates that royalty should be calculated in accordance with the Minerals Law. It is likely that amendments will be made to both the Law on Nuclear Energy and the Law on Minerals to ensure alignment and bring radioactive minerals back within the scope of the Minerals Law. This is the reason behind the reference in the working group's negotiation protocol, stating that "the parties have mutually agreed to establish and implement the CoG after the approval of the draft law amending the Law on Nuclear Energy and the Law on Minerals." In the event that uranium is included in the list of products for additional royalties, there is also the matter of calculating it. Minister Amarbayasgalan. D, the head of the working group, indicated that in the preliminary conditions of the IA, it was agreed that the base royalty would be 5%, Mongolian ownership would be replaced by a maximum limit of up to 5% for special royalty, which includes the increased royalty, resulting in a total of up to 19%. The working group has presented calculations demonstrating the public calculation of the royalty. This poses a conflict with the revised version of the Minerals Law, which is said to be under development. In the proposed revision, there is an alternative approach to calculating royalty, not based on total income, but rather derived from the difference in excess price. Should the additional royalty calculation exclusively consider the excess difference, the total calculation may indeed shift to 19 percent. This has raised an intricate issue wherein uranium is being singled out for specific treatment and estimation for public awareness. It's important to consider that changes in the law should not be viewed solely through the lens of a single investment or project, as this could potentially restrict opportunities for future projects and investments. To illustrate, it's worthwhile to recall that the increased royalties for copper at Oyu Tolgoi did not solely benefit Oyu Tolgoi but also had implications for Erdenet, ultimately affecting the economic feasibility of other copper projects. A broader perspective is essential when approaching changes in legislation, taking into account their impact on multiple projects and minerals.

UPCOMING IA AND UNRESOLVED TASKS

If we examine the pre-agreed principles of the agreement in light of the contentious issues that have arisen and continue to arise at Oyu Tolgoi, it might seem that all matters have been addressed. However, it's evident that attempts are being made to amend four different laws prior to finalizing the IA, much like what happened 14 years ago. This indicates that Mongolia hasn't adequately prepared for future agreements over the past decade. It's widely known that before concluding the Oyu Tolgoi IA, modifications were made to laws like the Water Law, Enterprise Income Tax Law, Highways Law, and other related legislation, with tax payments being frozen at the levels existing at the time of the contract's drafting. While alterations to the law before finalizing the Uranium CoG can be explained by the project not receiving tax incentives, the core issue lies in Mongolia's lack of readiness for investment agreements and a lack of strategic planning. Despite prolonged debates and controversies surrounding the establishment of IA for strategic deposits, Mongolia has yet to resolve these matters comprehensively. This indicates a failure to envision the future and manage the mining industry effectively. The inability to reform the Profitable Animals Law conceptually illustrates a fixation on today's IA, and there's an absence of a clear policy on how to deal with substantial mining investments. In a world where the shift toward clean energy is undeniable, the lack of a forward-looking policy for uranium, a primary source of nuclear energy and potentially a critical mineral deposit, is a missed opportunity. Following French President Emmanuel Macron's state visit to Mongolia in May, the country exhibited a sudden awakening. This is evident from the developments related to the IA. However, the sole leader of this government, Nyambaatar. Kh, who showed unwavering commitment, quickly handed over the negotiations to his minister after appointing him as the head of the working group. Under Nyambaatar. Kh's leadership, the Working Group engaged with investors for approximately five months, possibly even less, and was able to confirm, through a protocol during the return visit of the President of Mongolia to France, that the fundamental principles and general terms of the agreement had been pre-negotiated. On October 24, 2023, Orano Mining submitted its revised draft of the proposed project to the Mongolian side's Working Group. However, changing the head of the Working Group at such a crucial moment, when the agreement has not yet been finalized, is highly irresponsible. It's also a clear indication that the Mongolian government has not learned from past experiences. This could potentially lead to a reversal of the agreement or non-ratification. If the Working Group, following Nyambaatar. Kh, misses the window for conducting the IA negotiations, the likelihood of the IA not being approved may increase. There is significant apprehension within the working group and among the high-ranking officials of the participating states.

This fear is evident when discussing the positions of all parties involved regarding the agreement. The imprisonment of Bayartsogt. S, the architect of the Oyu Tolgoi IA, and Byambasaikhan. B, who was involved in the underground mine funding crisis, due to miscalculations has created an environment where officials may be inclined to protect themselves when facing difficulties. Some might even consider relinquishing their positions to avoid signing in anticipation of upcoming elections. Depending on the outcome of the investment agreement, it could be labeled as French or Russian espionage, potentially becoming a subject of public debate. Nonetheless, there is no turning back now. Once the working group has gained momentum, it must commit to maintaining the agreed conditions and work diligently to adhere to the pre-agreed timeline. Minister Amarbayasgalan. D, as the head of the working group, continues the courageous and strong leadership shown by Minister Nyambaatar. Kh. There are days left to roll up their sleeves and elevate the project's results to a new level. Although the basic terms and conditions have been pre-negotiated, the Working Group still has several steps ahead. Outstanding issues without mutual agreement, such as adjustments in financial modeling, mine closure regulations, terms and conditions for IA amendments, setting salary benchmarks for foreign and domestic staff, and more, need appropriate solutions to avoid potential social disputes. Additionally, amendments to the Laws on Minerals, Nuclear Energy, Investments, and Wealth Funds await approval by the Parliament, along with changes to the Shareholders' Agreement and Deposit Use Agreement, and the approval of the feasibility study.

NEGOTIATION TERMS WITH ORANO MINING

State Ownership: 1. The party acting on behalf of the Mongolian Government's share rights will be entitled to a 10% ownership of preferred shares, granted without any financial commitment or investment obligations. This arrangement ensures that preferential dividends will be received throughout the project's duration under pre-established conditions, regardless of the project's profitability, effectively mitigating future dividend-related risks. This is expected to yield approximately USD 400 million in total dividends. Furthermore, the project implementing company will hold exclusive veto power over alterations in the company's regulations and ownership.

Tax: 2. Concerning the ownership of preferred shares, the base royalty stands at 5%, with the Mongolian side's ownership being replaced by a specific percentage of the special royalty. Additionally, there is an agreement to include extra royalty, not specified in the prevailing law, with a predetermined calculation of the total royalty of up to 19%, contingent on market prices. Based on these royalty terms, it is projected that the project will contribute USD 50 million in royalty from annual sales of approximately USD 400 million. The pre-agreed royalty rate is set at a relatively higher level compared to other countries. For instance, Kazakhstan has 6 percent, Canada 5 percent, Australia 3.5 percent, and Uzbekistan 8 percent. No additional advantages, support, or preferential conditions beyond the existing tax law and legal framework in Mongolia will be granted. Consequently, the project is expected to generate USD 3.8 billion in tax revenue within the current tax system.

Regional Development: 3. The project's implementing company is committed to fostering economic growth in the Dornogovi province by generating new employment opportunities and facilitating the relocation of employees and their families to the region. As per the agreement, the company will collaborate with Dornogovi province and allocate USD 1 million annually during the operational phase of the project mine. This initiative is expected to result in the creation of approximately 700 new jobs.

Others: 4. A prior agreement has been reached to conduct all financial transactions linked to the purchase through a bank located in Mongolia. Additionally, it is stipulated that a minimum of 50 percent of the revenue from product sales will be processed through a bank established in Mongolia or a branch of a foreign bank registered in Mongolia.

Mining Insight Magazine, №10 (023)